Market news & analysis.

Catch up on the latest in the market and get the latest market reviews.

Forex

8 min read

USD hits 30-year high in 2024: What does it mean for the markets

26 Jun, 2026

Daily Forex Analysis

8 min read

A Traders Guide To Today's Federal Funds Rate Decision

12 Jun, 2025

Week Ahead

8 min read

Forex Trading Week Ahead Analysis: 10th June

09 Jun, 2025

Trading Strategies

8 min read

5 Signs That Indicate It’s Time to Change Your Trading Strategy

05 Jun, 2025

Trading Strategies

4 min read

How to Protect Yourself From Market Reversals?

05 Mar, 2025

Economic Indicator

7 min read

US Inflation Outlook for 2025

05 Mar, 2025

Week Ahead

5 min read

Forex Week Ahead Analysis: 3rd March

03 Mar, 2025

Economic Indicator

5 min read

How to Trade the ECB Rate Decision

03 Mar, 2025

Week Ahead

5 min read

Forex Week Ahead Analysis: 24th February

24 Feb, 2025

MetaTrader

8 min read

How to Subscribe to Trading Signals on MetaTrader

20 Feb, 2025

Cryptocurrencies

8 min read

Guide to Trump Coin: Everything Traders Must Know

19 Feb, 2025

Week Ahead

8 min read

Forex Week Ahead Analysis: 17th February

17 Feb, 2025

MetaTrader

6 min read

Advanced Technical Analysis with MT5 Indicators

14 Feb, 2025

Forex

8 min read

When to Trade a Forex Cross Pair?

13 Feb, 2025

Economic Indicator

8 min read

How Can Traders Use GDP to Find Opportunities?

11 Feb, 2025

Trading Strategies

4 min read

Can Positive Reevaluation Improve Your Trading Performance?

10 Feb, 2025

MetaTrader

7 min read

Can You Add Scripts to MetaTrader 4?

10 Feb, 2025

Week Ahead

8 min read

Forex Week Ahead Analysis: 10th February

10 Feb, 2025

Trading Strategies

8 min read

How to Avoid Being Influenced by Recency Bias

08 Feb, 2025

Economic Indicator

5 min read

DeepSeek's Disruption of Global Financial Markets: What You Need to Know

07 Feb, 2025

Trading Strategies

8 min read

Why You Should Set (And Stick To) A Maximum Trading Loss

07 Feb, 2025

MetaTrader

7 min read

How to Change The Volume of a Trade in MetaTrader

06 Feb, 2025

MetaTrader

6 min read

How To Create Templates In MT5

05 Feb, 2025

MetaTrader

8 min read

Mastering Chart Types in MetaTrader 5

04 Feb, 2025

Economic Indicator

7 min read

Trading Opportunities in the MSCI Emerging Markets Index

04 Feb, 2025

Economic Indicator

7 min read

What Happens When a Central Bank Cuts Interest Rates?

04 Feb, 2025

Forex

6 min read

A Comprehensive Guide to Using Demo Accounts + Top Tips

03 Feb, 2025

Week Ahead

5 min read

Forex Week Ahead Analysis: 3rd February

03 Feb, 2025

Economic Indicator

5 min read

Why European Central Bank Cut Interest Rates Again?

21 Jan, 2025

Economic Indicator

8 min read

Fed Cuts Interest Rates: Recession or Just a Soft Landing?

20 Jan, 2025

Week Ahead

5 min read

Forex Week Ahead Analysis: 20th January

20 Jan, 2025

Trading Strategies

8 min read

Treasury Bonds vs. Treasury Notes vs. Treasury Bills

17 Jan, 2025

Commodities

8 min read

What is WTI Crude Oil: A Beginner’s Guide to Understanding the Benchmark

14 Jan, 2025

Economic Indicator

8 min read

Impact of Fed Rate Cuts on Oil Prices

13 Jan, 2025

Week Ahead

5 min read

Forex Week Ahead Analysis: 13th January

12 Jan, 2025

Economic Indicator

8 min read

Where Interest Rates Might Go In 2025?

09 Jan, 2025

Cryptocurrencies

8 min read

Top Cryptocurrency Forecasts for 2025

08 Jan, 2025

Cryptocurrencies

8 min read

Bitcoin Price Prediction For 2025: What to Expect?

07 Jan, 2025

Forex

8 min read

Forex Markets in 2025: Top Predictions

07 Jan, 2025

Commodities

5 min read

Oil Prices in 2025: What Do The Experts Say?

07 Jan, 2025

Forex

8 min read

Emerging Market Currencies to Watch

26 Dec, 2024

Forex

8 min read

Should You Trade Forex During Christmas and New Year?

24 Dec, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 9th December

19 Dec, 2024

Commodities

6 min read

Will Gold Climb Higher in 2025?

19 Dec, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 16th December

18 Dec, 2024

Economic Indicator

5 min read

Is The US Recession Coming in 2025?

17 Dec, 2024

Economic Indicator

8 min read

Is the BOJ Interest Rate Hike Coming Soon?

16 Dec, 2024

Economic Indicator

7 min read

What are Corporate Bonds?

12 Dec, 2024

Economic Indicator

5 min read

What is next for FTSE 100?

11 Dec, 2024

Commodities

5 min read

Copper Trading: Capitalizing on Global Demand

09 Dec, 2024

Economic Indicator

6 min read

What is a Treasury Bond?

06 Dec, 2024

Economic Indicator

7 min read

Treasury Notes: Navigating Mid-Term US Debt Investments

05 Dec, 2024

Commodities

5 min read

Platinum Trading: Opportunities in Precious Metals

04 Dec, 2024

Economic Indicator

5 min read

How to Trade The MSCI World Index

21 Nov, 2024

Trading Strategies

6 min read

Advance-Decline Line: How to Use The Market Breadth Indicator

20 Nov, 2024

Trading Strategies

8 min read

Simple Moving Average (SMA)

19 Nov, 2024

Cryptocurrencies

5 min read

Crypto Staking - What it is And How it Works

11 Nov, 2024

Trading Strategies

10 min read

What is Position Trading?

09 Oct, 2024

Commodities

8 min read

Global Markets Stumble as Oil Prices Surge on Mideast Tensions

25 Sep, 2024

Trading Strategies

8 min read

Bullish and Bearish Harami Candlestick Pattern

24 Sep, 2024

Trading Strategies

8 min read

McClellan Summation Index: A Deep Dive

24 Sep, 2024

Trading Strategies

5 min read

Top Trend Following Strategies

24 Sep, 2024

Cryptocurrencies

5 min read

Yield Farming in Crypto: What Is It and How Does It Work?

24 Sep, 2024

Trading Strategies

5 min read

Beginner's Guide to Quantitative Trading

24 Sep, 2024

Cryptocurrencies

5 min read

Crypto Day Trading: Top Strategies

24 Sep, 2024

Trading Strategies

7 min read

How Does The Arms Index (TRIN) Analyzes Market Sentiment

24 Sep, 2024

Trading Strategies

8 min read

How to Use Put/Call Ratio to Gauge Market Sentiment

24 Sep, 2024

Economic Indicator

8 min read

Rate of Change (ROC) Indicator Explained

24 Sep, 2024

Forex

8 min read

Strategies for Trading Volatile Forex Pairs

24 Sep, 2024

Trading Strategies

6 min read

Why Use Custom Moving Averages To Tailor Your Strategy

24 Sep, 2024

Trading Strategies

8 min read

Buy and Hold: The Long-Term Trading Strategy

23 Sep, 2024

Trading Strategies

8 min read

Counter-Trend Trading: Strategies and Tips

23 Sep, 2024

Cryptocurrencies

5 min read

How to Use HODLing: The Long-Term Crypto Strategy

23 Sep, 2024

Trading Strategies

5 min read

Protective Put Strategy: The Complete Guide

23 Sep, 2024

Trading Strategies

5 min read

What is High-Frequency Trading (HFT) And How Does it Work?

23 Sep, 2024

Economic Indicator

5 min read

Dollar Retreats Ahead of US Jobs Report Looms

23 Sep, 2024

Trading Strategies

8 min read

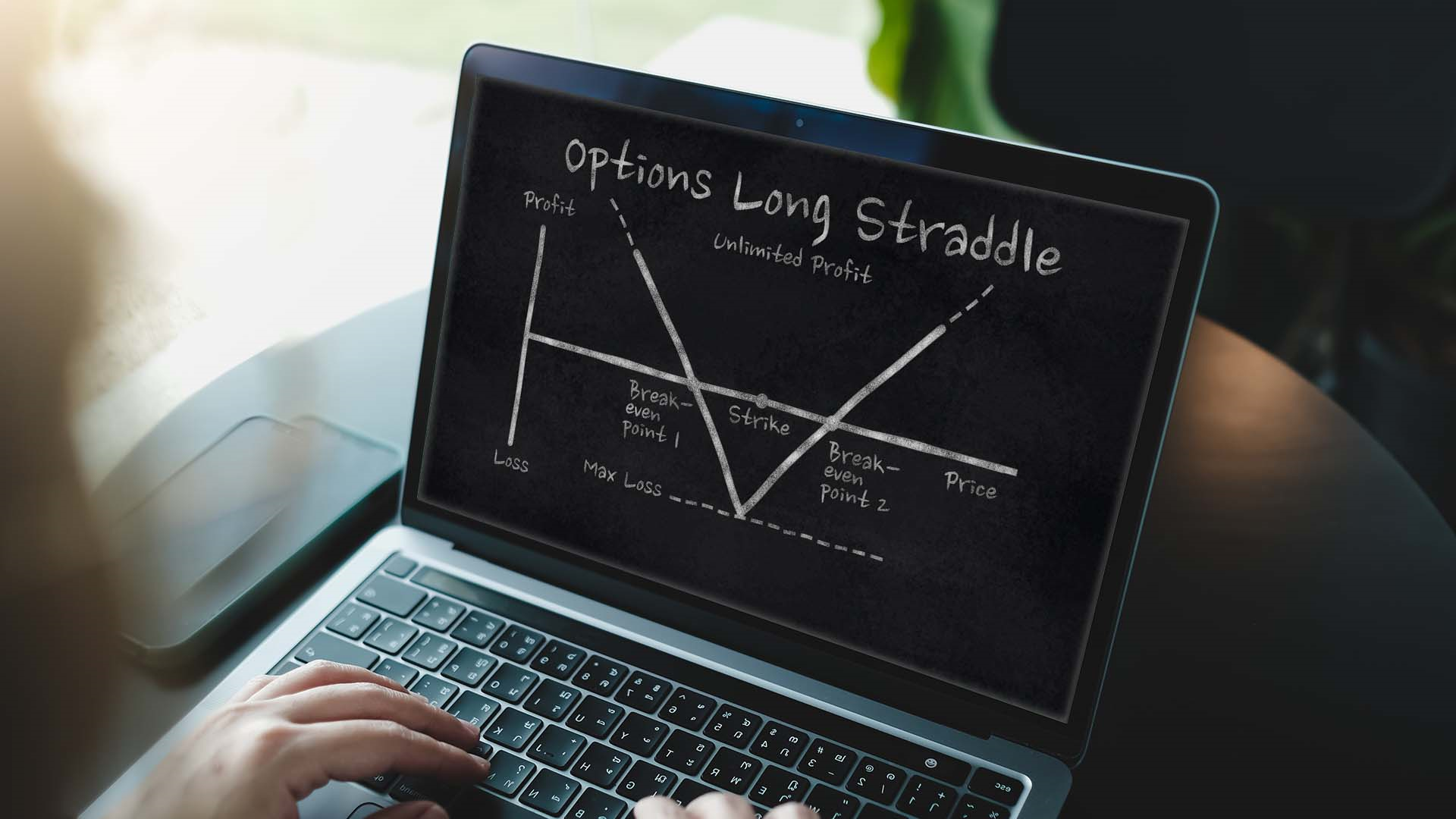

Straddle Options Strategy: Meaning, Examples and Benefits

23 Sep, 2024

Trading Strategies

5 min read

Technical Indicator Composites: The Complete Guide

23 Sep, 2024

Trading Strategies

6 min read

What is a Covered Call Options Strategy?

23 Sep, 2024

Forex

8 min read

What is a Take-Profit Order?

20 Sep, 2024

Forex

8 min read

How to Build Your Own Crypto Trading Strategy

19 Sep, 2024

Cryptocurrencies

5 min read

How to Create a Crypto Trading Journal

19 Sep, 2024

Cryptocurrencies

3 min read

How to Use Fundamental Analysis for Crypto Trading

19 Sep, 2024

Trading Strategies

5 min read

How to Use Rounding Top Pattern to Identify Bearish Signals

19 Sep, 2024

Trading Strategies

8 min read

Seasonal Trading: The Complete Guide

19 Sep, 2024

Trading Strategies

8 min read

Butterfly Pattern Trading: A Comprehensive Guide

18 Sep, 2024

Trading Strategies

8 min read

Diamond Trading Pattern: Comprehensive Guide for Traders

18 Sep, 2024

Trading Strategies

5 min read

Guide to Rounding Bottom Pattern

18 Sep, 2024

Trading Strategies

5 min read

How to Use Dark Cloud Cover to Identify Trading Signals

18 Sep, 2024

Commodities

How to Use Technical Analysis for Commodities Trading

18 Sep, 2024

Trading Strategies

8 min read

M Trading Pattern: Master Double Top Strategy

18 Sep, 2024

Trading Strategies

5 min read

Runaway Gap: Identifying and Trading Trends

18 Sep, 2024

Trading Strategies

8 min read

Top Indicators for Swing Trading

18 Sep, 2024

Trading Strategies

5 min read

Trading the Engulfing Pattern: Bullish & Bearish

18 Sep, 2024

Trading Strategies

5 min read

Trading the Piercing Line Pattern: A Quick Guide

18 Sep, 2024

Trading Strategies

8 min read

W Pattern Trading: Mastering the Double Bottom Strategy

18 Sep, 2024

Forex

7 min read

Dollar to Fluctuate as Investors Weigh Rate Cut Chances

18 Sep, 2024

Forex

5 min read

Forex and AI: How is AI Changing the Forex Market in 2024?

18 Sep, 2024

Commodities

5 min read

Gold Prices Falling After a Period of Strong Growth

18 Sep, 2024

Trading Strategies

5 min read

Questions to Ask When Trading Trends

18 Sep, 2024

Trading Strategies

8 min read

Top Ways to Minimize Missed Trades

18 Sep, 2024

Commodities

7 min read

USD to Range-Bound Amidst Central Bank Speculation

18 Sep, 2024

Trading Strategies

10 min read

Top Market Breadth Indicators

16 Sep, 2024

Trading Strategies

8 min read

Trading Wedge Pattern: A Comprehensive Guide

16 Sep, 2024

Week Ahead

5 min read

Forex Trading Week Ahead: 16th September

16 Sep, 2024

Trading Strategies

5 min read

Custom Oscillators To Personalizing Your Trading

10 Sep, 2024

Trading Strategies

8 min read

Forex Cycles Analysis: Timing Market Movements

10 Sep, 2024

Week Ahead

5 min read

Forex Trading Week Ahead: 9th September

09 Sep, 2024

Forex

5 min read

Exploring Exotic Forex Pairs: Opportunities and Risks

07 Sep, 2024

Economic Indicator

5 min read

Trading the Russell 2000: Everything You Should Know

05 Sep, 2024

Trading Strategies

5 min read

Pairs Trading: How to Use it For Hedging

05 Sep, 2024

Economic Indicator

5 min read

Commitment of Traders: What are COT Reports & How to Read them

04 Sep, 2024

Trading Strategies

8 min read

Exhaustion Gap: How to Trade the Final Push

04 Sep, 2024

Trading Strategies

5 min read

Understanding Common Gap in Trading

04 Sep, 2024

Daily Forex Analysis

5 min read

British Pound Reversal

29 Aug, 2024

Week Ahead

5 min read

Forex Trading Week Ahead: 26th August

26 Aug, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 26th August

26 Aug, 2024

Daily Forex Analysis

3 min read

How to trade GBP/JPY

22 Aug, 2024

Daily Forex Analysis

5 min read

Gold Makes New Highs

21 Aug, 2024

Week Ahead

5 min read

Forex Weekly Trading Ideas: 19th August

19 Aug, 2024

Week Ahead

5 min read

Forex Weekly Trading Ideas: 19th August (1)

19 Aug, 2024

Daily Forex Analysis

5 min read

Why are retail traders wrong?

19 Aug, 2024

Daily Forex Analysis

8 min read

GBP Rallies Despite Unemployment Claims Shock

14 Aug, 2024

Week Ahead

5 min read

Forex Weekly Trading Ideas: 12th August

12 Aug, 2024

CFD

5 min read

Japanese Markets to Rebound After its Biggest Drop in August's First Week

09 Aug, 2024

Shares

6 min read

Top Market Predictions for Q3 2024

07 Aug, 2024

Commodities

3 min read

Gold Trends for Q3 2024: What to Expect?

07 Aug, 2024

Daily Forex Analysis

2 min read

Navigating the EURUSD Ahead of ECB's Interest Rate Decision

07 Aug, 2024

Daily Forex Analysis

5 min read

Correction or Recession?

05 Aug, 2024

Week Ahead

8 min read

Weekly Forex Trading Ideas- 5th August

05 Aug, 2024

Daily Forex Analysis

5 min read

What a week to be a forex trader

02 Aug, 2024

Cryptocurrencies

8 min read

How to Use Technical Analysis When Trading Crypto

02 Aug, 2024

Trading Strategies

10 min read

How to Use The Umbrella Pattern Trading

01 Aug, 2024

Trading Strategies

10 min read

Dragon Pattern Trading: A Comprehensive Guide

29 Jul, 2024

Trading Strategies

8 min read

How to Use The Megaphone Trading Pattern

29 Jul, 2024

Week Ahead

8 min read

Forex Weekly Trading Ideas: 29th July

29 Jul, 2024

Trading Strategies

8 min read

Managing Emotions in High-Stakes Trading

29 Jul, 2024

Trading Strategies

4 min read

How to Overcome the Fear of Losing Your Gains

29 Jul, 2024

Daily Forex Analysis

5 min read

Weekly Forex Trading Ideas: 29th July

29 Jul, 2024

Trading Strategies

8 min read

Harmonic Trading Patterns

25 Jul, 2024

Daily Forex Analysis

8 min read

How To Trade USD/CAD: 24th July

25 Jul, 2024

Trading Strategies

7 min read

Triangle Pattern Trading: Master Technical Analysis

24 Jul, 2024

8 min read

How to Read Crypto Charts?

24 Jul, 2024

Trading Strategies

4 min read

How to Create a Trading Strategy

24 Jul, 2024

MetaTrader

7 min read

Can You Set Up Expert Advisors In Metatrader 4?

23 Jul, 2024

Week Ahead

5 min read

Forex Weekly Trading Ideas: 22nd July

21 Jul, 2024

Daily Forex Analysis

6 min read

How To Trade CoT Reports

17 Jul, 2024

MetaTrader

12 min read

How to Place a Trade on MT5

17 Jul, 2024

Week Ahead

5 min read

Forex Weekly Trading Ideas: 15th July

14 Jul, 2024

Daily Forex Analysis

10 min read

How to Achieve Consistent Wins in Forex Trading

12 Jul, 2024

Daily Forex Analysis

8 min read

Why Trading With Data Matters

10 Jul, 2024

Week Ahead

8 min read

Weekly Forex Trading Ideas: 8th July

07 Jul, 2024

Cryptocurrencies

8 min read

Top Indicators for Crypto Trading

05 Jul, 2024

Daily Forex Analysis

8 min read

Gold Finds Support Amid Rising Risk Events

04 Jul, 2024

Cryptocurrencies

8 min read

Effective Risk Management in Crypto Trading

02 Jul, 2024

Cryptocurrencies

8 min read

Cryptocurrency Trading Psychology: Everything Traders Should Know

02 Jul, 2024

Trading Strategies

8 min read

How to Setup the Perfect Trading Routine?

28 Jun, 2024

Trading Strategies

8 min read

How to Handle Trading Slumps

28 Jun, 2024

MetaTrader

8 min read

How to Set a Trailing Stop-Loss on MT5?

28 Jun, 2024

Cryptocurrencies

8 min read

How to Choose Optimal Time Frames for Crypto Trading

28 Jun, 2024

Cryptocurrencies

8 min read

Should You Trade Cryptocurrency on The Weekends?

27 Jun, 2024

MetaTrader

8 min read

How to Change Time Frames on MT5

27 Jun, 2024

MetaTrader

10 min read

How to Install Expert Advisors on MT5

27 Jun, 2024

Daily Forex Analysis

8 min read

Don't Trade EUR/AUD Until You See This

26 Jun, 2024

Commodities

8 min read

How Do Oil Prices Affect the Stock Market?

26 Jun, 2024

Trading Strategies

8 min read

What Is Implied Volatility & Factors Affecting it?

26 Jun, 2024

MetaTrader

8 min read

How to Create a Demo Account on MT5

24 Jun, 2024

Week Ahead

8 min read

Weekly Forex Trading Ideas: 24th June

23 Jun, 2024

Daily Forex Analysis

8 min read

How CoT Reports Could Predict a CAD Rally

19 Jun, 2024

Week Ahead

8 min read

Weekly Forex Trading Analysis: 17th June-21st June

16 Jun, 2024

Forex

6 min read

Benefits and Risks of investing in the Tokyo Stock Exchange from Vietnam

13 Jun, 2024

MetaTrader

6 min read

How To Use MetaTrader 5 Mobile App

07 Jun, 2024

Trading Strategies

8 min read

How to Use a Risk-Reward Calculator

06 Jun, 2024

Trading Strategies

8 min read

How to Trade With Point-and-Figure (P&F) Charts?

06 Jun, 2024

Trading Strategies

5 min read

Understanding the Dow Jones Index: A Beginner's Guide

06 Jun, 2024

Daily Forex Analysis

8 min read

ECB Poised to Cut Interest Rates

05 Jun, 2024

Trading Strategies

8 min read

How to Keep Trading Overconfidence in Check

05 Jun, 2024

Trading Strategies

8 min read

How To Find A Trading Style That Suits You

04 Jun, 2024

Forex

8 min read

How Forex Brokers Manage Risks

03 Jun, 2024

Week Ahead

9 min read

Forex Trading Week Ahead: 3rd June

02 Jun, 2024

Trading Strategies

8 min read

How to Use Pivot Points for Range Trading

30 May, 2024

Trading Strategies

6 min read

How to Trade With Guppy Multiple Moving Average (GMMA)

30 May, 2024

Daily Forex Analysis

5 min read

Donald Trump Found Guilty- FX Unchanged

30 May, 2024

Daily Forex Analysis

Why Silver is the Undervalued Commodity

29 May, 2024

Forex

7 min read

5 Exit Strategies To Consider in Forex Trading

28 May, 2024

Forex

EUR/USD Price Forecast 2024: What to Expect

28 May, 2024

MetaTrader

8 min read

Trading Cryptocurrencies with MetaTrader 5

28 May, 2024

Daily Forex Analysis

GBP/USD Spikes as UK Inflation Declines to 2.3%

22 May, 2024

Daily Forex Analysis

4 min read

GBPUSD A Key Pair to Watch This Week for Forex Traders

20 May, 2024

Economic Indicator

7 min read

What is a Floating Exchange Rate?

17 May, 2024

Trading Strategies

6 min read

How to Backtest a Trading Strategy?

17 May, 2024

Forex

6 min read

How to Trade the EUR/CHF

16 May, 2024

Forex

8 min read

How to Trade GBP/CAD?

16 May, 2024

Daily Forex Analysis

3 min read

US CPI: A Market Letdown and Its Implications

15 May, 2024

Daily Forex Analysis

2 min read

Insights Ahead of US CPI Release

14 May, 2024

Daily Forex Analysis

5 min read

Sell In May and Go Away

08 May, 2024

Trading Strategies

5 min read

How do Bank Holidays Affect Trading Prices?

02 May, 2024

Economic Indicator

6 min read

How Does The FOMC Affect The Market?

02 May, 2024

Forex

8 min read

How to Trade AUD/JPY

02 May, 2024

Trading Strategies

3 min read

How to Bounce Back From a Blown Trading Account

02 May, 2024

Trading Strategies

10 min read

How to Use The Dragonfly Doji Candlestick Pattern?

02 May, 2024

Daily Forex Analysis

5 min read

To Trade or Fade USDCAD?

29 Apr, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 29th April

28 Apr, 2024

Trading Strategies

5 min read

What is the ICT trading strategy?

26 Apr, 2024

Forex

5 min read

What is a Lot in Forex?

26 Apr, 2024

Daily Forex Analysis

5 min read

USDJPY: Can Price Go Any Higher?

24 Apr, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 22nd April

21 Apr, 2024

Trading Strategies

5 min read

Difference Between Trading on Demo Accounts and Live Accounts

19 Apr, 2024

Trading Strategies

8 min read

Reasons Why New Traders Give up Too Early

19 Apr, 2024

Daily Forex Analysis

3 min read

GBPUSD Traders Be Aware

17 Apr, 2024

Economic Indicator

8 min read

The Complete Guide to Global Financial Regulatory Bodies

17 Apr, 2024

Trading Strategies

5 min read

How to Overcome Trading Anxiety

16 Apr, 2024

Economic Indicator

8 min read

Top Financial Regulatory Bodies in Europe

16 Apr, 2024

Daily Forex Analysis

5 min read

USDCAD Outlook Amidst Diverging Central Bank Policies

15 Apr, 2024

Forex

8 min read

How to Prepare Your Taxes as a Forex Trader in 2024

15 Apr, 2024

Week Ahead

8 min read

Forex Week Ahead Analysis: 15th April

14 Apr, 2024

Daily Forex Analysis

2 min read

Keeping an Eye on USDCHF Amidst Central Bank Moves and Economic Data

09 Apr, 2024

Week Ahead

3 min read

Forex Week Ahead Analysis: 8th April

08 Apr, 2024

Daily Forex Analysis

3 min read

Gold Rallies Amidst Rising US Bond Yields: A Technical Outlook

03 Apr, 2024

Trading Strategies

5 min read

5 Ways to Start Forex Trading As a Beginner

02 Apr, 2024

Week Ahead

3 min read

Forex Week Ahead Analysis: 1st April

01 Apr, 2024

Daily Forex Analysis

3 min read

Understanding Japan's Stance on JPY Weakening

27 Mar, 2024

Daily Forex Analysis

3 min read

WTI Crude Oil Set to Trade to $100.00?

26 Mar, 2024

Daily Forex Analysis

3 min read

Navigating the Forex Markets: A Quieter Week Ahead

25 Mar, 2024

Daily Forex Analysis

3 min read

How To Trade GBPUSD Fundamentals

21 Mar, 2024

Daily Forex Analysis

3 min read

USD In Focus Ahead Of Fed Announcement

20 Mar, 2024

MetaTrader

5 min read

Optimizing MT4 and MT5 Performance with VPS: Configuration Tips and Tricks

19 Mar, 2024

Week Ahead

3 min read

Forex Week Ahead Analysis: 18th March

18 Mar, 2024

Forex

3 min read

Common Mistakes to Avoid When Making Forex Deposits

18 Mar, 2024

Forex

5 min read

How to Transition from a Demo Account to a Live Account

18 Mar, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 18th March 2025

17 Mar, 2024

Forex

5 min read

Why Do Forex Brokers Charge Commission Fees?

13 Mar, 2024

Trading Strategies

6 min read

Top Gap Trading Strategies

12 Mar, 2024

Forex

4 min read

Demo Accounts: Setting Goals and Establishing Rules

12 Mar, 2024

Daily Forex Analysis

4 min read

Exploring the Recent Plunge of USDJPY: Is Further Decline Imminent?

11 Mar, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 11th March

11 Mar, 2024

Trading Strategies

5 min read

How to Trade Inside Days

08 Mar, 2024

Trading Strategies

5 min read

Passive vs Active Trading: What's the Difference?

08 Mar, 2024

Daily Forex Analysis

5 min read

Is EURUSD Bullish In 2024?

06 Mar, 2024

Forex

3 min read

What are Speed Resistance Lines?

05 Mar, 2024

Trading Strategies

8 min read

What is The Aroon Indicator?

05 Mar, 2024

Forex

8 min read

Yield Curve: What it is and How to Use it

05 Mar, 2024

Forex

10 min read

How to Trade USD/MXN Currency Pair

05 Mar, 2024

Forex

10 min read

How to Use The Slow Stochastic Oscillator for Day Trading

05 Mar, 2024

Forex

5 min read

What Are Price Charts (And How to Use Them?)

05 Mar, 2024

Forex

8 min read

What is the Linear Regression Slope?

05 Mar, 2024

Trading Strategies

3 min read

How to Trade with CCI Indicator

04 Mar, 2024

MetaTrader

8 min read

How to Start Trading on MetaTrader 4 with Robots

04 Mar, 2024

Economic Indicator

8 min read

How Does Supply and Demand Affect Markets?

04 Mar, 2024

Trading Strategies

8 min read

What is the Raff Channel Indicator?

04 Mar, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 4th March

03 Mar, 2024

Daily Forex Analysis

5 min read

Bitcoin Soars as New ETFs Drive Record Trades

29 Feb, 2024

Daily Forex Analysis

5 min read

Tips For Trading Gold

27 Feb, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 26th February

25 Feb, 2024

Trading Strategies

6 min read

What is an Emerging Market?

21 Feb, 2024

Daily Forex Analysis

5 min read

AUDJPY In Focus Ahead Of RBA Meeting Minutes

19 Feb, 2024

Forex

5 min read

What to do With Big Wins as a Forex Trader?

19 Feb, 2024

Week Ahead

8 min read

Forex Week Ahead Analysis: 19th Feb | Technical Analysis

18 Feb, 2024

Trading Strategies

6 min read

5 Key Strategies for Advanced Technical Analysis

16 Feb, 2024

Trading Strategies

10 min read

What is the Hidden Divergence Trading Strategy?

15 Feb, 2024

Trading Strategies

5 min read

What is the 5-3-1 Trading Strategy in Forex?

15 Feb, 2024

Trading Strategies

8 min read

How to Set Realistic Trading Goals

14 Feb, 2024

Trading Strategies

5 min read

How to Learn From Your Trading Mistakes With Technical Analysis

14 Feb, 2024

Daily Forex Analysis

5 min read

Will Gold Prices Fall Further?

14 Feb, 2024

Trading Strategies

8 min read

Five Trading Strategies For a Highly Volatile Market

13 Feb, 2024

4 min read

How to Build Flexibility in Forex Trading

13 Feb, 2024

MetaTrader

7 min read

How to Check Your Trade History in MT5?

13 Feb, 2024

Forex

5 min read

What Does it Take to Cultivate a Winning Attitude for Forex Trading

13 Feb, 2024

Forex

7 min read

Why Forex Traders Should Use a Risk Calculator

13 Feb, 2024

Trading Strategies

5 min read

How to Combine Trading Strategies

12 Feb, 2024

Forex

5 min read

How and When to Buy or Sell in Forex Trading

12 Feb, 2024

Forex

8 min read

How to Trade Low Volatility Markets?

12 Feb, 2024

Week Ahead

8 min read

Forex Week Ahead Analysis: 12th Feb | EURUSD | GBPUSD | SILVER

11 Feb, 2024

Daily Forex Analysis

3 min read

Have Traders Spotted This Forex Breakout?

07 Feb, 2024

Daily Forex Analysis

7 min read

A Blueprint to Consistency in Forex Trading

05 Feb, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 5th February | Technical Analysis

04 Feb, 2024

Daily Forex Analysis

3 min read

USD Index Key Levels

31 Jan, 2024

Daily Forex Analysis

3 min read

Don't Trade GBP/AUD Until You See This

29 Jan, 2024

Week Ahead

8 min read

Forex Week Ahead Analysis: 27th January

28 Jan, 2024

Week Ahead

8 min read

Forex Week Ahead Analysis: 29th Jan | Technical Analysis

28 Jan, 2024

Forex

8 min read

Three-Bar Reversal Pattern For Day Trading

26 Jan, 2024

Trading Strategies

5 min read

What is the Retail Sales Index?

26 Jan, 2024

Forex

6 min read

A Forex Trader's Guide to Federal Reserve Bank

26 Jan, 2024

Forex

8 min read

How to Trade the EUR/JPY Currency Pair?

26 Jan, 2024

Trading Strategies

8 min read

How Trading Competitions Work?

26 Jan, 2024

Cryptocurrencies

8 min read

The Year Ahead: Top Crypto Predictions for 2024

26 Jan, 2024

Forex

6 min read

What Are Competitive Spreads?

26 Jan, 2024

Daily Forex Analysis

3 min read

EURJPY What Next? | Price Action Trading

24 Jan, 2024

Daily Forex Analysis

5 min read

Is This The NEXT Trending Forex Pair?

22 Jan, 2024

Week Ahead

8 min read

Forex Week Ahead Analysis: 22nd Jan | Technical Analysis

21 Jan, 2024

MetaTrader

6 min read

How to Download Historical Data on MT4

17 Jan, 2024

Economic Indicator

6 min read

What is the Consumer Sentiment Index?

17 Jan, 2024

Daily Forex Analysis

5 min read

Will This Market Crash?

17 Jan, 2024

Economic Indicator

JPY Forecast For 2024

15 Jan, 2024

Economic Indicator

5 min read

Understanding the Link Between Trade and Capital Flows

15 Jan, 2024

Daily Forex Analysis

3 min read

Where Is The Bitcoin Price Heading Now?

15 Jan, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 15th Jan | Technical Analysis

14 Jan, 2024

Daily Forex Analysis

5 min read

Price Action Trading In Forex

10 Jan, 2024

Forex

8 min read

Top Triangle Chart Patterns

09 Jan, 2024

Commodities

8 min read

Gold Price Forecast For 2024

09 Jan, 2024

Economic Indicator

5 min read

How Does The Bank of England Impact The Forex Market?

09 Jan, 2024

Forex

10 min read

What is Leverage in Forex?

09 Jan, 2024

Forex

2 min read

How To Predict Forex Movements?

08 Jan, 2024

Forex

5 min read

What is The Tick Volume Indicator?

08 Jan, 2024

Daily Forex Analysis

5 min read

Forex Traders Alert! EURGBP Technical Analysis

08 Jan, 2024

Forex

7 min read

How Setting The Right Position Sizing Can Save Traders?

08 Jan, 2024

Trading Strategies

8 min read

Trading Biases vs Predictions: What's The Difference?

08 Jan, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 8th Jan | Technical Analysis

07 Jan, 2024

Daily Forex Analysis

5 min read

Master Trading The Range In Forex | In The Trading Zone

03 Jan, 2024

Economic Indicator

5 min read

Forex Economic Calendar 2024: What to Watch

02 Jan, 2024

Shares

10 min read

Popular Stocks to Start Your 2024 Out Strong

02 Jan, 2024

Week Ahead

5 min read

Forex Week Ahead Analysis: 2nd Jan | Technical Analysis

01 Jan, 2024

Trading Strategies

8 min read

How to Avoid Stop-Loss Hunting?

27 Dec, 2023

Forex

8 min read

Helpful Tips For Forex Trading Newbies

27 Dec, 2023

Forex

8 min read

How to Trade AUD/USD?

27 Dec, 2023

Forex

8 min read

How to Use a Forex Demo Account for Practice?

27 Dec, 2023

Trading Strategies

5 min read

How to Manage Currency Exposure in Your Portfolio?

26 Dec, 2023

MetaTrader

8 min read

Trading with MetaTrader's Forex Volume Indicator

26 Dec, 2023

Trading Strategies

5 min read

What is Drawdown in Forex Trading?

26 Dec, 2023

Forex

8 min read

Forex Predictions 2024: Trends Shaping the Future of Forex Markets

26 Dec, 2023

Forex

8 min read

How to Trade the Impact of Politics on Forex Markets?

26 Dec, 2023

Forex

5 min read

Why Does the BoJ Intervene in the Forex Markets?

26 Dec, 2023

Trading Strategies

5 min read

Top Tips to Resume Trading After The 2023 Christmas Break

20 Dec, 2023

Trading Strategies

8 min read

Top Trading Strategies For GBP/USD

20 Dec, 2023

Economic Indicator

5 min read

What Higher Oil Prices in 2024 Could Mean For The Markets?

20 Dec, 2023

Trading Strategies

8 min read

What is Golden Cross Trading?

18 Dec, 2023

Daily Forex Analysis

4 min read

How To Find Better Forex Trading Levels

18 Dec, 2023

Economic Indicator

5 min read

2024 Economy And Stock Market Predictions

15 Dec, 2023

Trading Strategies

5 min read

How to Trade a Short Squeeze?

15 Dec, 2023

Forex

3 min read

How Bond Yields Affect Currency Movements in Forex?

15 Dec, 2023

Partnership

8 min read

How to attract Clients to your Introducing Brokers (IBs) Business through Social Media?

15 Dec, 2023

Cryptocurrencies

5 min read

How to Invest in Crypto Without Buying Crypto?

15 Dec, 2023

Trading Strategies

4 min read

How To Set A Stop-Loss Based On Price Volatility?

15 Dec, 2023

Forex

8 min read

Is Forex Trading Halal or Haram?

14 Dec, 2023

Cryptocurrencies

4 min read

How To Cautiously Trade Cryptocurrencies?

13 Dec, 2023

Daily Forex Analysis

5 min read

How To Be A Better Forex Trader | In The Trading Zone

13 Dec, 2023

Partnership

3 min read

Top 8 Questions Introducing Brokers Need to Ask When Selecting a Broker

11 Dec, 2023

Trading Strategies

8 min read

What is The Marubozu Candlestick Pattern?

11 Dec, 2023

Economic Indicator

5 min read

What is The Petrodollar?

11 Dec, 2023

Trading Strategies

4 min read

How to Know When to Close a Trade

11 Dec, 2023

Forex

8 min read

What is the Risk-Reward Ratio?

11 Dec, 2023

Daily Forex Analysis

3 min read

How To Use Currency Strength Vs Weakness In Forex Trading

27 Nov, 2023

Partnership

5 min read

What is an Introducing Broker (IB)?

24 Nov, 2023

Forex

3 min read

How to Calculate Lot Size in Forex?

23 Nov, 2023

Economic Indicator

8 min read

How Do Unemployment Rates Affect The Forex Market?

23 Nov, 2023

Forex

3 min read

4 Big Mistakes Traders Make When Setting Stops

23 Nov, 2023

Forex

5 min read

Choosing Forex Pairs: A Comprehensive Guide

23 Nov, 2023

Forex

5 min read

How to Study Your Losses to Realize Gains?

23 Nov, 2023

Trading Strategies

5 min read

Scalping vs. Position Trading: Which is Right for You?

23 Nov, 2023

Economic Indicator

5 min read

Understanding the Relationship Between Oil and Currency

23 Nov, 2023

Daily Forex Analysis

5 min read

Risk On Returns In The Forex Markets

22 Nov, 2023

Forex

3 min read

What The Israel-Palestine Conflict Means For Forex Markets?

17 Nov, 2023

Economic Indicator

5 min read

How Does Inflation Affect The Interest Rates?

15 Nov, 2023

Trading Strategies

5 min read

Online Trading vs Offline Trading: What's the Difference?

15 Nov, 2023

Forex

5 min read

When to Move from Demo to Live Forex Trading Account?

15 Nov, 2023

Forex

5 min read

How to Read and Leverage The Forex Economic Calendar

14 Nov, 2023

Trading Strategies

5 min read

What Are Trading Signals & How Do They Work?

14 Nov, 2023

Forex

5 min read

Forex Trading and Taxes: What You Need to Know

13 Nov, 2023

Forex

5 min read

Understanding Supply and Demand in Forex Trading

13 Nov, 2023

CFD

8 min read

What is the FRA40 index?

10 Nov, 2023

Forex

5 min read

How Central Banks Impact the Forex Market?

07 Nov, 2023

Forex

5 min read

How to Maintain Forex Trading Discipline and Patience?

07 Nov, 2023

Forex

5 min read

How to Read And Understand Forex Trading Quotes

07 Nov, 2023

Trading Strategies

5 min read

What is Multi-Asset Trading?

07 Nov, 2023

Trading Strategies

5 min read

A Beginner's Guide to Hedging

07 Nov, 2023

Trading Strategies

8 min read

How to Use a Trading Journal?

07 Nov, 2023

Trading Strategies

8 min read

Top Strategies to Trade The Euro/British Pound

06 Nov, 2023

Forex

8 min read

Forex Trading Hours: What is The Right Time to Trade?

27 Oct, 2023

Forex

5 min read

The Forex Trader's Guide to USD/JPY Pair

26 Oct, 2023

Economic Indicator

5 min read

Major Economic Reports That Affect the British Pound

26 Oct, 2023

Forex

7 min read

The Impact of BOJ on the Forex Market

26 Oct, 2023

Trading Strategies

8 min read

How to Create an AI Trading Bot With ChatGPT?

25 Oct, 2023

Trading Strategies

3 min read

Benefits And Risks of Using AI in Trading

18 Oct, 2023

Forex

5 min read

How to Switch Forex Brokers?

18 Oct, 2023

Forex

8 min read

How to Trade the Euro/British Pound?

18 Oct, 2023

Forex

3 min read

How to Trade the EUR/AUD Currency Pairs?

17 Oct, 2023

Forex

8 min read

How to Trade the Japanese Yen?

17 Oct, 2023

CFD

5 min read

FTSE 100 vs FTSE 250: What’s The Difference?

16 Oct, 2023

Trading Strategies

8 min read

Risks Associated With Candlestick Chart Patterns

16 Oct, 2023

Trading Strategies

5 min read

Stop-Loss Strategy For Day Trading

16 Oct, 2023

Forex

5 min read

Five Questions to Ask Your Forex Broker

16 Oct, 2023

Trading Strategies

5 min read

Hedging vs Speculation: Top Differences

10 Oct, 2023

Forex

3 min read

How to Use ChatGPT for Algorithmic Trading?

10 Oct, 2023

Daily Forex Analysis

3 min read

How To Analyze A Forex Chart: AUDJPY In Focus

10 Oct, 2023

Commodities

5 min read

The Correlation Between Commodities And Inflation

10 Oct, 2023

CFD

5 min read

What is the NAS100 Index?

09 Oct, 2023

Trading Strategies

5 min read

Risk Management Strategies for Active Traders

05 Oct, 2023

Trading Strategies

5 min read

Risks of Automated Trading Systems

04 Oct, 2023

Forex

4 min read

How to Make the Most of Your Brokerage Account

04 Oct, 2023

Forex

5 min read

How Does GDP Affect Forex Trading?

02 Oct, 2023

Economic Indicator

5 min read

How to Read a Balance Sheet For Trading?

02 Oct, 2023

Forex

5 min read

What Are the Factors Affecting USD/CAD?

02 Oct, 2023

Forex

8 min read

How Oil Impacts The Canadian Dollar?

02 Oct, 2023

CFD

5 min read

CFDs vs Futures: What Are The Differences?

20 Sep, 2023

Forex

8 min read

What is Forex VPS Hosting: A Comprehensive Guide

08 Sep, 2023

CFD

8 min read

How to Trade Crypto CFDs?

08 Sep, 2023

Economic Indicator

5 min read

How Does CPI Affect the Stock Market?

06 Sep, 2023

Commodities

8 min read

How Does NFP Affect the Price of Gold?

06 Sep, 2023

Forex

5 min read

Seasonal Market patterns For EUR/USD

06 Sep, 2023

Forex

5 min read

Top Differences Between Hedging and Stop-loss

06 Sep, 2023

Trading Strategies

8 min read

What is the Ideal Setup for Trading?

06 Sep, 2023

CFD

5 min read

Top Industries in FRA40 Index

06 Sep, 2023

CFD

5 min read

The Complete Guide to Euro Stoxx 50 Index

05 Sep, 2023

CFD

5 min read

What is DAX 30 Index?

05 Sep, 2023

Commodities

8 min read

What is OPEC, and How Does it Influence Oil Prices?

25 Aug, 2023

Trading Strategies

5 min read

How Will AI Impact Trading

24 Aug, 2023

Commodities

8 min read

How Can Oil Prices Affect Stock Prices?

23 Aug, 2023

Trading Strategies

4 min read

How to Use ChatGPT For Trading?

10 Aug, 2023

Forex

8 min read

Top AI Tools for Trading

10 Aug, 2023

Economic Indicator

5 min read

How Does GDP Affect the Stock Market?

09 Aug, 2023

Forex

5 min read

Forex Economic Calendar for 2023

31 Jul, 2023

Economic Indicator

5 min read

What is Core PCE and How Does it Affect the Forex Market?

31 Jul, 2023

Economic Indicator

5 min read

Top Economic News Events for Forex Trading

25 Jul, 2023

Forex

5 min read

What is Volatility Index (VIX) And How Do You Trade It?

25 Jul, 2023

Forex

8 min read

S&P 500 Index

20 Jul, 2023

Forex

8 min read

How Does The Recession Affect The Stock Market?

18 Jul, 2023

Forex

5 min read

What is ADP National Employment Report?

18 Jul, 2023

Forex

5 min read

What is the Shanghai Index?

18 Jul, 2023

Forex

5 min read

How Does Inflation Affect the Forex Market?

13 Jul, 2023

MetaTrader

7 min read

How To Get The News Feed In MT4?

12 Jul, 2023

MetaTrader

6 min read

How To Set Up MetaTrader? Step-By-Step Instruction

11 Jul, 2023

MetaTrader

3 min read

Can You Use MetaTrader 4 Without A Broker?

07 Jul, 2023

MetaTrader

7 min read

How to Copy a Trade on MT4?

07 Jul, 2023

MetaTrader

6 min read

Is MetaTrader 4 Good For Beginners?

07 Jul, 2023

MetaTrader

5 min read

How to Add Templates to MT4?

05 Jul, 2023

MetaTrader

10 min read

Type of Orders in Metatrader

30 Jun, 2023

MetaTrader

8 min read

How To Speed Up MT4?

29 Jun, 2023

Forex

8 min read

Understanding the Fear and Greed Index: A Comprehensive Guide for Forex Traders

29 Jun, 2023

MetaTrader

8 min read

How Do You Set Price Alerts With MetaTrader 4?

21 Jun, 2023

MetaTrader

5 min read

How Does MetaTrader 4 Work?

21 Jun, 2023

MetaTrader

8 min read

How to Add Commodities to MT4?

21 Jun, 2023

MetaTrader

2 min read

How to Add Indices to MT4?

21 Jun, 2023

Forex

8 min read

Understanding the Japanese Stock Market: Insights for Vietnamese Investors

20 Jun, 2023

MetaTrader

How to Use MetaTrader 4

19 Jun, 2023

Forex

5 min read

Dos and Don'ts of Forex Trading in Vietnam

18 Jun, 2023

Forex

8 min read

What is Nikkei 225?

18 Jun, 2023

Forex

5 min read

Managing Risk When Investing in the Tokyo Stock Exchange from Vietnam

15 Jun, 2023

Forex

4 min read

How to Open a Trading Account to Invest in the Tokyo Stock Exchange from Vietnam

15 Jun, 2023

Forex

5 min read

Top Industries to Invest in on the Tokyo Stock Exchange for Vietnamese Investors

12 Jun, 2023

Forex

4 min read

Common Mistakes When Exchanging Foreign Currency to Vietnamese Dong

09 Jun, 2023

Forex

5 min read

Tips on Exchange Rate When Exchanging Foreign Currency to Vietnamese Dong

07 Jun, 2023

Forex

5 min read

What traders need to know about fees when exchanging foreign currency to Vietnamese dong

07 Jun, 2023

Forex

4 min read

5 Guides for Exchanging Foreign Currency to Vietnamese Dong Without Getting Scammed

05 Jun, 2023

Forex

7 min read

The Ultimate Guide to The Tokyo Stock Exchange

02 Jun, 2023

Forex

5 min read

Exchanging Foreign Currency to Vietnamese Dong: Pros And Cons

01 Jun, 2023

MetaTrader

13 min read

Basic Functions of MT4

23 May, 2023

MetaTrader

8 min read

Customizing MT4 Interface: Tips and Tricks

23 May, 2023

MetaTrader

5 min read

Top 10 Essential MT4 Indicators for Technical Analysis

09 May, 2023

MetaTrader

8 min read

The Advantages of Using MT4 for Forex Trading

09 May, 2023

MetaTrader

10 min read

A Comprehensive Guide to MT4 Trading for Beginners

01 May, 2023

MetaTrader

7 min read

How to Optimize MT4 Trading Experience

01 May, 2023

Trading Strategies

5 min read

What is Purchasing Manager's Index?

24 Apr, 2023

Trading Strategies

8 min read

15 Strongest Currencies in The World

17 Apr, 2023

Forex

5 min read

A Beginner's Guide to Exchanging Foreign Currency to Vietnamese Dong

06 Apr, 2023

Trading Strategies

4 min read

Buying The Dip: What Does it Mean?

16 Mar, 2023

Trading Strategies

5 min read

Popular Trading Tools for New Traders

07 Mar, 2023

Commodities

5 min read

Gold Price Forecast for 2023

05 Mar, 2023

Daily Forex Analysis

3 min read

Forex Chart Of The Day: Is Gold Heading To $1800.00?

22 Feb, 2023

MetaTrader

8 min read

How to Open a MetaTrader 5 Account

15 Feb, 2023

Trading Strategies

5 min read

Automated Trading vs Manual Trading

08 Feb, 2023

Commodities

5 min read

Top Factors That Affect Gold Prices

23 Jan, 2023

Forex

5 min read

How to Become a Part-Time Forex Trader

19 Jan, 2023

Forex

5 min read

Top Forex Trends For 2023

10 Jan, 2023

Trading Strategies

8 min read

The Ultimate CFD Day Trading Guide

21 Dec, 2022

Cryptocurrencies

8 min read

Cryptocurrencies to Focus on in 2023

06 Dec, 2022

Trading Strategies

5 min read

What is Grid Trading?

01 Dec, 2022

Trading Strategies

5 min read

Russian Ruble Financial Crisis 2022: What to Expect?

22 Nov, 2022

Trading Strategies

5 min read

How Do Interest Rates Affect The Stock Market?

15 Nov, 2022

Trading Strategies

8 min read

What is a Ranging Market?

08 Nov, 2022

Trading Strategies

3 min read

How to Use RSI for Intraday Trading

02 Nov, 2022

Trading Strategies

8 min read

How to Trade With MetaTrader Webtrader

26 Oct, 2022

Trading Strategies

6 min read

How to Build a Diversified Portfolio

18 Oct, 2022

Forex

8 min read

Top Forex Forecasting Techniques

11 Oct, 2022

Trading Strategies

5 min read

What is Dow Jones?

26 Sep, 2022

Trading Strategies

8 min read

What is Overtrading (And How to Avoid it)

19 Sep, 2022

Trading Strategies

5 min read

How to Master The Psychology of Forex Trading

06 Sep, 2022

Forex

8 min read

Major Forex Market Hours and Trading Sessions

30 Aug, 2022

CFD

4 min read

How to Choose a CFD Trading Platform

23 Aug, 2022

Trading Strategies

4 min read

How to Overcome Fear When Trading

22 Aug, 2022

Forex

5 min read

The Most Volatile Currency Pairs (& How to Trade Them)

08 Aug, 2022

Trading Strategies

6 min read

What is Carry Trade in Forex?

03 Aug, 2022

Forex

5 min read

How to Trade Forex News: Forex News Trading Strategy

27 Jul, 2022

Trading Strategies

5 min read

Why Do Traders Lose Money in Intraday Trading

19 Jul, 2022

Forex

5 min read

What is Consolidation in the Stock Market?

12 Jul, 2022

Forex

8 min read

Forex Words and Jargons Every Trader Should Know

28 Jun, 2022

Trading Strategies

5 min read

What Are Market Reversals And How to Spot Them?

07 Jun, 2022

Trading Strategies

10 min read

MetaTrader 4: Top Tips and Tricks

01 Jun, 2022

Forex

8 min read

Hawkish vs Dovish: How Do They Affect The Forex Market

23 May, 2022

Cryptocurrencies

5 min read

Cryptocurrency vs Forex Market: What’s The Difference?

09 May, 2022

Commodities

5 min read

Top Silver Trading Strategies To Get Ahead

03 May, 2022

Forex

8 min read

What Are The Key Drivers of The Forex Market

25 Apr, 2022

Daily Forex Analysis

5 min read

Questions to Ask When Planning Trade Exits

06 Apr, 2022

Forex

5 min read

7 Popular Indices Trading Strategies

21 Mar, 2022

Forex

5 min read

Non-Farm Payrolls and Forex: Everything You Need to Know

14 Mar, 2022

Forex

5 min read

How The Russia-Ukraine Crisis is Impacting the Forex Market

08 Mar, 2022

CFD

5 min read

Top CFD Trading Strategies For Beginners

01 Mar, 2022

Commodities

5 min read

Trading Gold CFDs: Here’s Everything You Need to Know

21 Feb, 2022

Forex

5 min read

How to Use the USDX for Forex Trading

16 Feb, 2022

Forex

6 min read

What is Margin Call in Forex (And How Do You Avoid One)

08 Feb, 2022

Commodities

3 min read

How to Trade Oil CFDs

25 Jan, 2022

CFD

5 min read

How Does an Index CFD Work?

13 Jan, 2022

CFD

5 min read

10 Important Rules for CFD Trading

21 Dec, 2021

Forex

10 min read

15 Most Popular Forex Chart Patterns

09 Dec, 2021

Forex

4 min read

How to Find Out Which Forex Broker Is Legit

24 Nov, 2021

Shares

3 min read

Index Trading Explained: How to Trade Indices

22 Nov, 2021

Commodities

8 min read

Silver Trading: A Beginner's Guide to Trading in Silver

18 Nov, 2021

Cryptocurrencies

5 min read

Top 10 Tips for Bitcoin and Crypto Trading

10 Nov, 2021

Shares

5 min read

Short Selling Stocks: What does Shorting a Stock Mean?

26 Oct, 2021

Forex

5 min read

16 Effective Day Trading Strategies for Beginners

19 Oct, 2021

Commodities

5 min read

Oil Trading: How to Trade Oil Spot Prices, Options, and Futures

11 Oct, 2021

Cryptocurrencies

5 min read

Get Started with Cryptocurrency CFDs: Everything You Need to Know

04 Oct, 2021

Forex

8 min read

Forex 101: Terms And Jargon That You Need To Understand

01 Oct, 2021

Shares

5 min read

CFDs vs Stocks: Which is a Better Investment?

21 Sep, 2021

Commodities

2 min read

How to Start Oil Trading in 5 Simple Steps

13 Sep, 2021

Forex

5 min read

Top Economic Indicators Traders Should Watch

08 Sep, 2021

Forex

8 min read

Forex Trading Strategies That Actually Work

31 Aug, 2021

Forex

5 min read

How to Use Trailing Stop-Loss in Forex: 3 Powerful Techniques

31 Aug, 2021

Commodities

8 min read

How to Trade Commodities: A Complete Guide

24 Aug, 2021

Forex

8 min read

Top 5 Moving Average Trading Indicators

24 Aug, 2021

Cryptocurrencies

5 min read

What is Bitcoin and How Do You Trade It?

20 Aug, 2021

Forex

8 min read

Types of Forex Charts (And How to Read Them)

12 Aug, 2021

Commodities

8 min read

How to Trade Gold: Top Gold Trading Strategies and Tips

11 Aug, 2021

Daily Forex Analysis

5 min read

FOREX Chart Of The Day: How To Identify A Market To Trade

11 Aug, 2021

Forex

8 min read

Top 10 Trading Indicators Every Forex Trader Should Know

06 Aug, 2021

Forex

7 min read

A Guide to Multiple Timeframe Analysis

05 Aug, 2021

CFD

5 min read

Top Benefits of Trading CFDs

30 Jul, 2021

Commodities

5 min read

How to Start Day Trading Gold

29 Jul, 2021

CFD

8 min read

A Beginner's Guide to Contract for Differences (CFDs)

21 Jul, 2021

Forex

8 min read

6 Forex Exit Indicators: When to Exit Your Trade and Take a Profit

16 Jul, 2021

Forex

7 min read

How Interest Rates Affect Forex Trading

16 Jul, 2021

Forex

5 min read

Why Forex Traders Need Quantitative Tightening

02 Jul, 2021

Forex

5 min read

Why A Forex Trading Plan Matters (And How To Build One)

01 Jul, 2021

Forex

7 min read

Trend Trading In Forex: How To Effectively Use This Strategy

25 Jun, 2021

Forex

6 min read

What Is Algorithmic Trading

11 Jun, 2021

Forex

5 min read

Spoofing In Forex Trading Blueberry Markets

10 Jun, 2021

Forex

5 min read

Monetary And Fiscal Policies In Forex

06 Jun, 2021

Forex

5 min read

How To Profit From Double Candlestick Patterns

04 Jun, 2021

Forex

3 min read

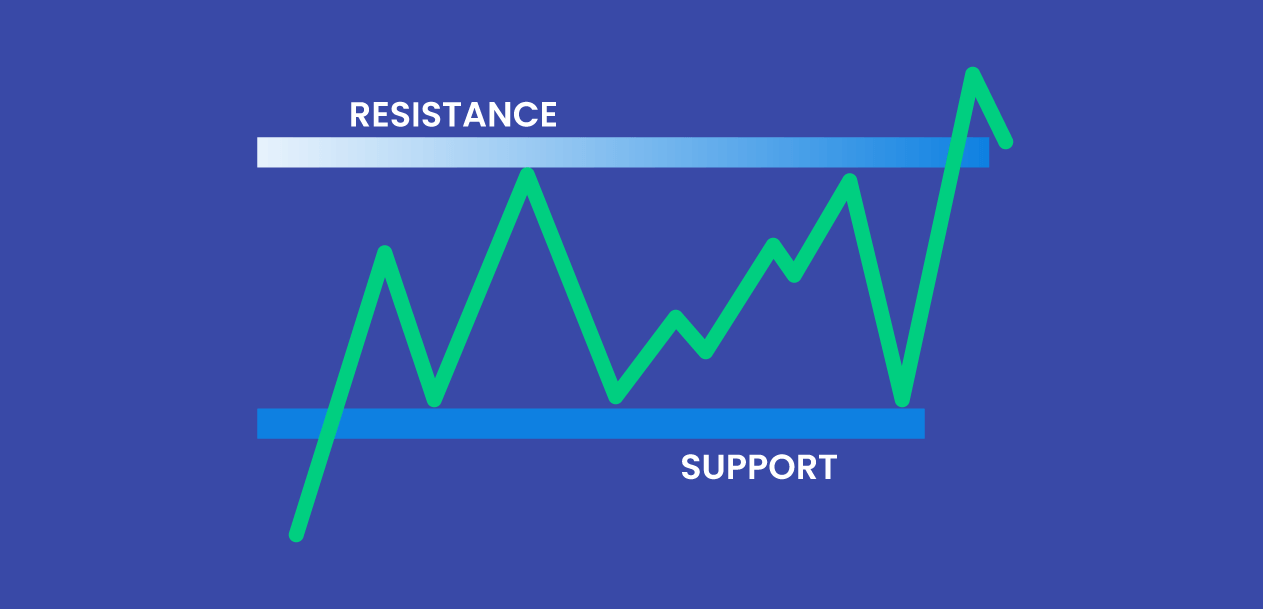

Forex Trading Using Support And Resistance Levels

21 May, 2021

Forex

5 min read

How to Use a VPS For Forex?

21 May, 2021

Cryptocurrencies

5 min read

Can Bitcoin Eventually Become (Or Replace) The US Dollar As A Reserve Currency?

14 May, 2021

Forex

5 min read

Exploring Binary Options Trading

14 May, 2021

Forex

5 min read

Three Powerful Strategies You Can Use In Forex Trading

30 Apr, 2021

Forex

5 min read

Binni Ong On The Past, Present, And Future Of Forex

28 Apr, 2021

Forex

5 min read

Trading With The RSI Indicator

09 Apr, 2021

Forex

5 min read

It's always a good time to make your money work for you

01 Apr, 2021

Forex

4 min read

Choosing Your Forex Broker

18 Mar, 2021

Forex

5 min read

The Best Time To Trade Forex

15 Mar, 2021

Forex

8 min read

The Pip And Its Usage In Forex

12 Feb, 2021

Forex

5 min read

The Basics Of A Fundamental Analysis

11 Feb, 2021

Forex

5 min read

The Basics Of Opening A Forex Account

09 Feb, 2021

Forex

5 min read

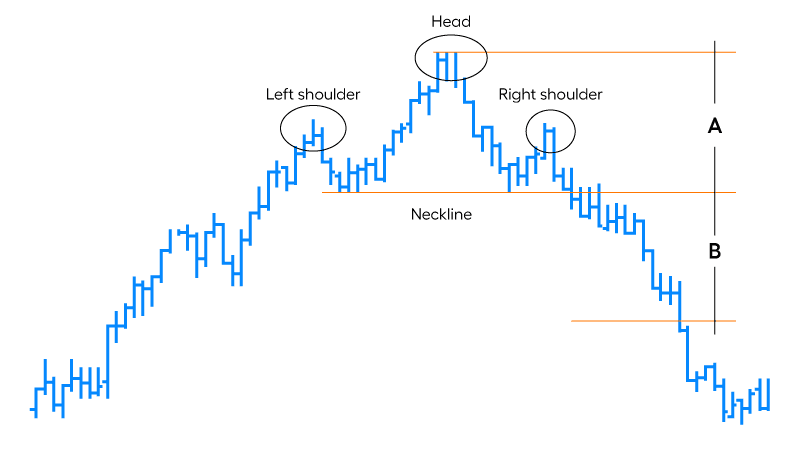

How To Trade With The Head And Shoulders Pattern

05 Feb, 2021

Forex

8 min read

Forex: Its History And Futures

03 Feb, 2021

Forex

5 min read

The Basics Of Swing Trading

25 Jan, 2021

Forex

8 min read

Forex 101: What You Need To Know Before Placing Your First Trade

20 Jan, 2021

Forex

8 min read

Forex 101: How To Make A Forex Trading Plan

12 Jan, 2021

Trading Strategies

8 min read

Divergence Trading and How to Navigate Around It

29 Dec, 2020

Daily Forex Analysis

6 min read

How To Use The RSI Indicator Forex Trading

09 Dec, 2020

Daily Forex Analysis

5 min read

How To Spot Trend In The FOREX Market

03 Dec, 2020

Trading Strategies

5 min read

Trading with the Head and Shoulders Pattern

06 Oct, 2020

Trading Strategies

5 min read

Pivot Points and Why They Matter

02 Oct, 2020

Trading Strategies

5 min read

The Key to Making It as a Retail Trader

12 Sep, 2019

Trading Strategies

8 min read

The Nitty-Gritty of Risk Management

12 Sep, 2019

Page 1 of 1